Neobanks have successfully disrupted the finance sector by leveraging technology to improve the customer journey, so they can match the experience delivered by the latest generation of apps like Amazon and Uber. Research by the Financial Conduct Authority (FCA) shows that Starling and Monzo, despite only receiving authorisation in 2016 and 2017 respectively, have already built their share of the UK personal account market to 8%. This growth has been largely driven by digitally-savvy younger consumers attracted by their mobile offering.

The business model of several neobanks originally relied on basic banking products such as current and savings accounts, lending and money transfers. However, neobanks have expanded their ranges to include higher-margin offerings- for instance, Starling’s Personal Finance Marketplace gives customers access to insurance, mortgages and investments.

Investments are a particularly attractive proposition due to the sheer size of the market. According to Boston Consulting Group’s latest Global Asset Management Report, the asset management industry grew by 11% in 2020 to $103 trillion. Retail investors, who hold $42 trillion of assets under management (AUM), have led this growth.

Democratization of investments

The democratization of the investment industry is well underway, as demonstrated in early 2021 by the traders who congregated at Reddit’s WallStreetBets forum and took on the professionals holding short positions in stocks like Gamestop.

A survey published in 2020 by financial services solutions provider Broadridge showed how participation is expanding. The share of the Mass Market- those with less than $100,000 to invest- grew from 30% in 2017 to 38% in 2020. Meanwhile, the Mass Affluent and High Net Worth segments stagnated or marginally declined. Millennials were the fastest-growing cohort, rising from 9% in 2017 to 14% in 2020. Together, Millennials and Generation X accounted for over 40% of the overall market.

One of the biggest drivers of this trend has been the lowering and elimination of trading fees, making the stock market much more accessible to retail investors. Silicon Valley-based Robinhood- the favoured broker of the WallStreetsBets traders- was a pioneer, offering commission-free trading on stocks and exchange traded funds (ETFs) when it launched in 2014. According to its latest results, Robinhood had 17.3 million monthly active users in December 2021 and $98 billion AUM. UK rival Freetrade is on a similar trajectory, if not quite as spectacular. Having released its app in 2018, the company revealed in October 2021 that it had reached one million users.

The major players were slow to react, but they eventually had to follow suit. Charles Schwab, among the world’s biggest brokers with nearly 33 million accounts and just short of $8 trillion AUM (as of December 2021), announced it would eliminate fees in 2019. Around the same time, Interactive Brokers, currently with 1.73 million accounts and over $350 billion AUM, launched its IBKR Lite platform offering free trading on US stocks and ETFs.

Opportunity for neobanks to add investments

According to research conducted by Huddlestock in March 20221, despite the scale of the opportunity, less than half of European consumer neobanks have introduced an investment proposition. Only 44% of Europe’s top neobanks offer investments to their customers, with 54% listing more than one asset class. Funds are the most common, followed by ETFs, stocks and cryptocurrency.

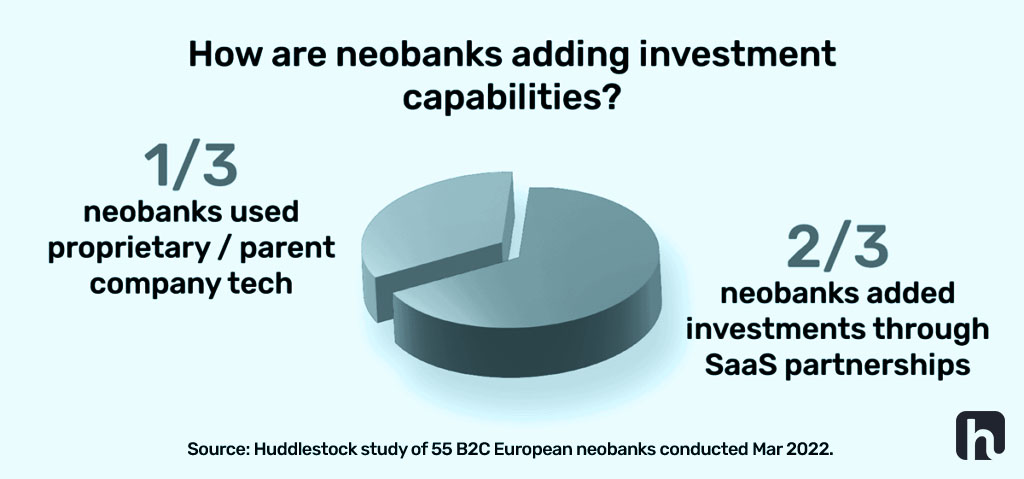

The neobanks offering investment products have adopted different business models. Two thirds have partnered with Investment-as-a-Service solutions like Huddlestock, leveraging the underlying infrastructure to go to market quickly and keep costs to a minimum. One third of neobanks, meanwhile, utilise proprietary or parent company technology, and notably, most of these were owned by large incumbent banks.

To draw a conclusion from this research, neobanks are supporting the further democratization of investing, but many haven’t tapped into this sizeable income stream yet. Even among those that have, 46% have scope to increase their offering from a single asset class. One particular area of growth is sustainable investing, where Huddlestock’s research showed that one quarter of neobanks provided such an offering. Dutch neobank Bunq launched an ESG product in February, to be followed shortly by Germany-based Tomorrow.

Barriers to entry

While the opportunity seems enticing, launching an investment proposition isn’t without challenges.

Time to market: the timescale involved is typically measured in years. The software and infrastructure required to manage investments are complex, and neobanks rarely have the in-house expertise to build it, let alone ensure it meets regulatory requirements.

Licensing– Few neobanks secure licenses to carry out investments because of the demanding application process, timeline and fees.

Regulatory requirements– Ensuring a fintech stays on the right side of regulations like the Markets in Financial Instruments Directive (MiFID) requires significant resources. Failure to do so risks heavy penalties- the US Financial Industry Regulatory Authority (FINRA) fined Robinhood $70 million in June 2021 for outages and misleading customers when market volatility spiked at the start of the pandemic.

Build vs partner vs buy

Neobanks have three options when it comes to adding investments to their product range.

Building a solution in–house may grant greater control over design and implementation, but the time to market is very slow and this demands significant resources.

Partnering with a third-party investment provider presents a quicker route to market but less flexibility because neobanks are tied to the partner’s product, brand and revenue share or commercial agreement.

Buying a dedicated investment SaaS solution provides the best of both worlds – a quick route to market and complete flexibility over design, so a neobank can offer a broad investment proposition and enhance or make changes at any time. What’s more, owning the solution means the neobank receives all the revenue.

The arguments in favour of buying a SaaS solution were strong enough to persuade Revolut and Lunar, while Swedish fintechs Alwy and Sigmastocks recently decided to work with Huddlestock.

Investment as a Service

Neobanks are perfectly positioned to introduce investments to their product range, so we expect an increasing number to enter this space. Barriers to entry exist, but Application Programming Interfaces (APIs) facilitate integration, allowing neobanks to add the necessary capabilities quickly and easily.

To learn more about Huddlestock’s Investment as a Service, get in touch today.

1 Research carried out by Huddlestock in March 2022 by analysing 81 neobanks with headquarters in Europe, based on a NeoBanks.app list plus five additional companies known to Huddlestock. Pre-launch, B2B and kids/teenager neobank companies were excluded from the final analysis, leaving a sample size of 55. All investment product data including asset classes was sourced from the neobanks’ own websites or apps. Data pertaining to investment/SaaS partnerships was sourced from neobanks’ websites and press releases.